THE MIDDLE PATH TO SUSTAINABILITY: REFRAMING ESG THROUGH THE LENS OF BUDDHIST ECONOMICS

คำสำคัญ:

Applied Buddhism, Buddhism and Sustainable Development, Buddhist Economics, Ethical Governance ESG, Comparative Ethical Mapping Framework (CEMF)บทคัดย่อ

Background and Objectives: Environmental, Social, and Governance (ESG) has become a standard reference in corporate sustainability discourse. Despite its rapid diffusion, ethical reasoning within ESG frameworks is often left implicit, with social and environmental concerns justified primarily through compliance, reputation, or risk management. This study examines a persistent ethical gap in contemporary ESG frameworks by focusing on how moral intention is treated,

or left implicit, within prevailing sustainability practices. Rather than evaluating ESG performance, the study aims to clarify why existing ESG architectures struggle to internalize ethical reasoning within organizational decision-making. To address this gap, the paper develops the Comparative Ethical Mapping Framework (CEMF), which places core ESG strategic domains in dialogue with an ethical logic drawn from Buddhist economics, particularly principles associated with the Noble Eightfold Path. The analysis is conceptual in scope and does not involve empirical testing or the proposal of new reporting standards.

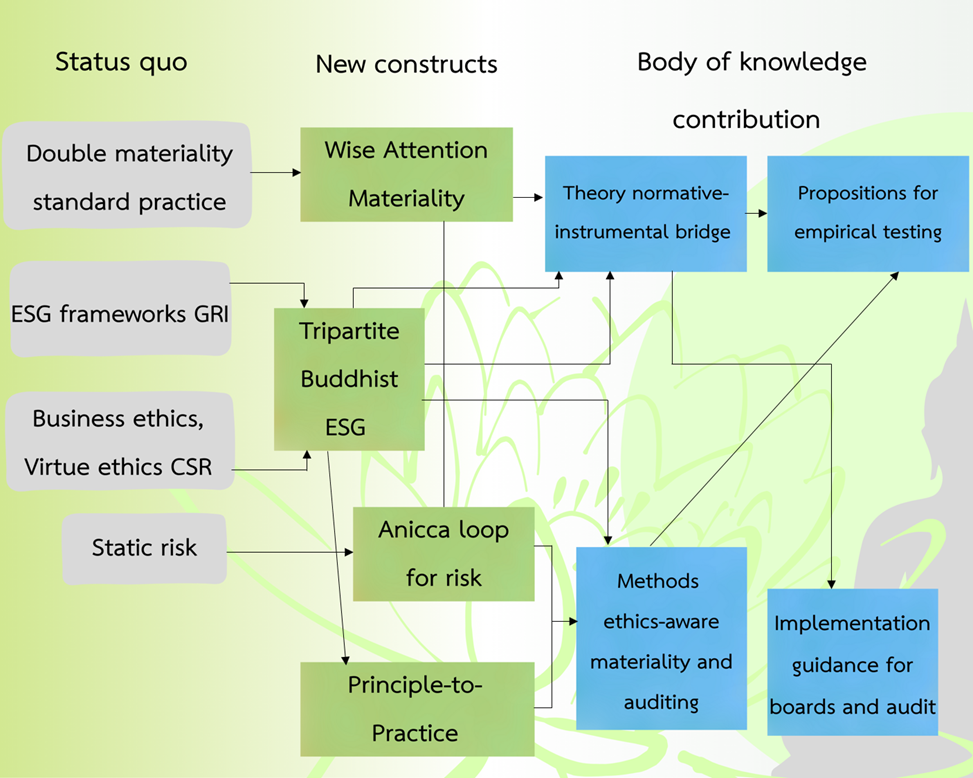

Methodology: The study was conceptual and interpretive. It drew on a thematic review of ESG-related scholarship published between 2015 and 2024, from which a set of representative studies was selected for closer analysis. On this basis, the paper developed the Comparative Ethical Mapping Framework (CEMF). The framework placed six ESG domains alongside selected Buddhist ethical concepts, including ethical conduct (Sīla), right livelihood (Sammā-ājīva), loving-kindness (Mettā), wisdom (Paññā), and impermanence (Anicca). The aim was not to produce a new metric, but to examine how ethical reasoning is embedded, displaced,

or constrained within existing ESG structures.

Main Results: The analysis showed that ethical considerations were not treated consistently across ESG domains. Governance and disclosure practices tended to emphasize formal procedures and outward accountability, while ethical conduct was often assumed rather than examined. In the areas of risk management and stakeholder engagement, ESG practices frequently focus on anticipation, mitigation, or legitimacy, with limited attention to impermanence and relational responsibility. These patterns pointed to a recurring tension between managerial rationality and ethical reflection. To clarify this tension, the paper developed a Buddhist-ESG interpretive structure that linked observable practices to ethical principles and to intention (Cetanā)

as understood in Buddhist thought.

Involvement to Buddhadhamma: Grounded in Buddhist economics, this study engages Buddhadhamma as an ethical and ontological foundation rather than as a symbolic supplement, positioning the analysis within the field of Applied Buddhism and its contribution to Buddhism and sustainable development. Core Buddhist concepts, including impermanence (Anicca),

non-self (Anattā), and wise attention (Yoniso Manasikāra), are mobilized to interrogate ESG practices directly, treating organizational action as ethically consequential conduct shaped by intention and interdependence. In this way, the paper applies Buddhist ethical reasoning to contemporary sustainability challenges, demonstrating how ontological insights from Buddhism expose the limits of prevailing ESG assumptions. For example, impermanence (Anicca) challenges the view of risk as an anomaly to be controlled, emphasizing uncertainty as an inherent condition of economic life, while wise attention (Yoniso manasikāra) redirects materiality assessment away from purely financial salience toward forms of moral urgency that may not yet be visible in financial statements.

Conclusions: The paper offered a Buddhist economic reading of ESG that placed ethical intention at the center of familiar sustainability domains. It suggested implications for how responsibility, risk, and engagement are understood in organizational contexts, and identified areas where further conceptual and empirical work may be needed. Further work is needed to examine how ethical orientation influences ESG processes empirically and whether it is associated with more durable forms of organizational change.

เอกสารอ้างอิง

Amos, R. (2025). A Critical Analysis of the Global Biodiversity Framework. Journal of International Wildlife Law & Policy, 28(2), 123-192. https://doi.org/10.1080/13880292.2025.2539577.

Boiral, O. (2013). Sustainability reports as simulacra? A counter-account of A and A+ GRI reports. Accounting, Auditing & Accountability Journal, 26(7), 1036-1071. https://doi.org/10.1108/AAAJ-04-2012-00998.

Brown, C. (2017). Buddhist Economics: An Enlightened Approach to the Dismal Science. New York, United State of America: Bloomsbury Publishing.

Cho, C. H., Michelon, G., Patten, D. M. & Roberts, R. W. (2015). CSR disclosure: The more things change…? Accounting, Auditing & Accountability Journal, 28(1), 14-35. https://doi.org/10.1108/AAAJ-12-2013-1549.

Daniels, P. L. (2010a). Climate change, economics and Buddhism-Part I: An integrated environmental analysis framework. Ecological Economics, 69(5), 952-961. https://doi.org/10.1016/j.ecolecon.2009.12.002.

Daniels, P. L. (2010b). Climate change, economics and Buddhism-Part 2: New views and practices for sustainable world economies. Ecological Economics, 69(5), 962-972. https://doi.org/10.1016/j.ecolecon.2010.01.012.

Eccles, R. G., Ioannou, I. & Serafeim, G. (2014).The Impact of Corporate Sustainability on Organizational Processes and Performance.Management Science, 60(11), 2835-2857. https://doi.org/10.1287/mnsc.2014.1984.

Edmans, A. (2022). The end of ESG. Financial Management, 52(1), 3-17. https://doi.org/10.1111/fima.12413.

Freeman, R. E., Harrison, J. S. & Wicks, A. (2007). Managing for Stakeholders: Survival, Reputation, and Success. New Haven, United State of America: Yale University Press.

Garcia-Torea, N., Fernandez-Feijoo, B. & De La Cuesta, M. (2016). Board of director's effectiveness and the stakeholder perspective of corporate governance: Do effective boards promote the interests of shareholders and stakeholders? BRQ Business Research Quarterly, 19(4), 246-260. https://doi.org/10.1016/j.brq.2016.06.001.

Grewal, J. & Serafeim, G. (2020). Research on Corporate Sustainability: Review and Directions for Future Research. Foundations and Trends® in Accounting, 14(2), 73-127. https://doi.org/10.1561/1400000061.

GRI. (2020). Consolidated set of GRI sustainability reporting standards 2020. Amsterdam, Netherlands: GRI.

Ioannou, I. & Serafeim, G. (2014). The impact of corporate social responsibility on investment recommendations:Analysts' perceptions and shifting institutional logics. Strategic Management Journal, 36(7), 1053-1081. https://doi.org/10.1002/smj.2268.

ISSB. (2023). Sustainability-related risks and opportunities and the disclosure of material information. London, United of Kingdom: IFRS Foundation.

Khan, M., Serafeim, G. & Yoon, A. (2016). Corporate Sustainability: First Evidence on Materiality. The Accounting Review, 91(6), 1697-1724. https://doi.org/10.2308/accr-51383.

Kotsantonis, S. & Serafeim, G. (2019). Four Things No One Will Tell You About ESG Data. Journal of Applied Corporate Finance, 31(2), 50-58. https://doi.org/10.1111/jacf.12346.

Loy, D. R. (2003). The Great Awakening: A Buddhist Social Theory. New York, United State of America: Wisdom Publications.

Manetti, G. (2011). The quality of stakeholder engagement in sustainability reporting: empirical evidence and critical points. Corporate Social Responsibility and Environmental Management, 18(2), 110-122. https://doi.org/10.1002/csr.255.

Nidumolu, R., Prahalad, C. K. & Rangaswami, M. R. (2009). Why Sustainability Is Now the Key Driver of Innovation. Harvard Business Review, 87(9), 57-64.

Porter, M. E. & Kramer, M. R. (2011). Creating shared value. Harvard Business Review, 89(1-2), 62-77.

SASB. (2017). SASB Conceptual Framework. San Francisco, United State of America: Sustainability Accounting Standards.

Ven. P. A. Payutto. (1992). Buddhist Economics: A Middle Way for the market Place. Bangkok, Thailand: Buddhadhamma Foundation.

Walls, J. L. & Berrone, P. (2017). The Power of One to Make a Difference: How Informal and Formal CEO Power Affect Environmental Sustainability. Journal of Business Ethics, 145, 293-308. https://doi.org/10.1007/s10551-015-2902-z.

Zhang, L-S. (2025). The impact of ESG performance on the financial performance of companies: evidence from China's Shanghai and Shenzhen A-share listed companies. Frontiers in Environmental Science, 13, 1507151. https://doi.org/10.3389/fenvs.2025.1507151.

ดาวน์โหลด

เผยแพร่แล้ว

รูปแบบการอ้างอิง

ฉบับ

ประเภทบทความ

สัญญาอนุญาต

ลิขสิทธิ์ (c) 2025 วารสารมานุษยวิทยาเชิงพุทธ

อนุญาตภายใต้เงื่อนไข Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.