Cost and the Return on Mattress OTOP Product of Ban Nongyarak Community in Pudsa Subdistrict, Mueang District, Nakhon Ratchasima Province

DOI:

https://doi.org/10.14456/nrru-rdi.2024.3Keywords:

Cost and Return, One Tambon One Product (OTOP), Picnic Mat, Community ProductAbstract

Participating in informing entrepreneurs about operations, allow them to manage value-added and risk appropriately. Leading to research with objectives were: 1) to study production costs, 2) to study return from production, and 3) to analyze costs and returns in producing a One Tambon One Product (OTOP) item, specifically the 3.5 feet, 5 feet, and 6 feet Picnic Mattresses in the Nongyarak community, Phutsa Sub-District, Mueang District, Nakhon Ratchasima Province. This qualitative research used a specific target group of 11 people selected through structured interview questionnaires that had an index of item-objective congruence between questions and research objectives ranging from 0.67-1.00. Data were collected using in-depth individual interviews conducted in the field, and workshop meetings were held to analyze costs and returns and to prepare profit and loss statements. Content analysis was used to summarize phrases and sentences from interviews, and descriptive statistics were used to find percentages. Financial ratios were used to analyze relationships between cost and return data.

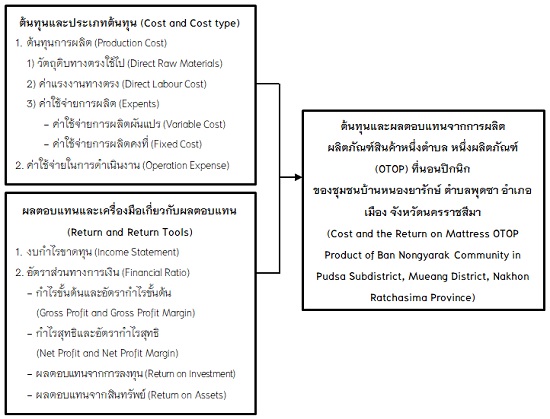

The research findings revealed that 1) overall image of production costs totaling 2,138,576 Baht per year. Direct raw material costs were the cost of poly fabric, synthetic fibers, thread, and needles totaling 910,000 Baht per year. Direct labour costs included costs from sewing and cutting, synthetic fiber filling, and mattress edging, totaling 455,000 Baht per year. Expents consisted of water, electricity, and oil costs totaling 618,310 Baht per year, and operational costs were packaging bag and sticker costs totaling 58,000 Baht per year. 2) Returns from production showed revenue from sales of 2,600,000 Baht per year, averaging 1,850 Baht per unit per year. 3) Gross profit was 520,024 Baht per year with a gross profit margin of 20.00%. Net profit was 461,424 Baht per year with a net profit margin of 17.75%. Return on investment calculated to 559.25%, and return on assets was 76.90%. Therefore, this information could be used as a importance process that businesses need to be aware of in order to manage resources appropriately, create reliable financial, and profit reports continuously for sustainable business growth.

References

Abhisitpinyo, B. (2012).Cost Accounting 1. SE-Education.

Armart, S. (2023). Management of Production Quality Control Systems Costs, and Returns for Sisaketshallot Production in Accordance with Thai Geographical Indication Product Standard of Shallot Farmers in Sisaket Province. Journal of Management and Development Ubon Ratchathani Rajabhat University, 10(1), 1-19.

Chaiyakham, S., Sriyong, P., Boonlert, R., Boriboonmangsa, S., & Kasala, C. (2020). Cost and Return Analysis of Pounded Unripe Rice Production: Case Study of Operator in Ban Klangyai, Klangyai Sub-District, Banphue District, Udonthani Province. Research Report. Faculty of Management Science, Udon Thani Rajabhat University.

Chantawanich, S. (2022). Qualitative Research Methods (26th ed.). Chulalongkorn University Press.

Chaowana, P., Tuncharo, S., & Konggachod, A. (2021). An Analysis for Cost and Return on Investment from Rice Farms of the Farmers in Rattaphum District, Songkhla Province. Research Report. Rattaphum College, Rajamangala University of Technology Srivijaya.

Federation of Accounting Professions Building Under Royal Patronage. (2015). The Elements of Financial Statements. In Manual explaining the Conceptual Framework for Financial Reporting. https://www.tfac.or.th/upload/9414/IhJcrKfW69.pdf

Gulick, L., & Urwick, L. (1973). The Science of Administration. Columbia University.

Hasan, S. I., Saeed, H. S., Al-Abedi, T. K., & Flayyih, H. H. (2023). The role of target cost management approach in reducing costs for the achievement of competitive advantage as a mediator: an applied study of the iraqi electrical industry. International Journal of Economics and Finance Studies, 15(2), 214-230. Doi: 10.34109/ijefs.202315211

Kemmis, A., & Taggart, R. (2010). The Action research planner. Deakin University.

Office of the National Economic and Social Development Council. (2016). Project of Development of a statistical data system and indicators for government administration according to the national strategy: Issue 16 grassroots economy. Academic Service Center of Chulalongkorn University.

Official statistice registrations syttems. (2022, 13 December). Population in 2022. Download village level statistics: Nong Yarak Village, Phutsa Subdistrict, Mueang District, Nakhon Ratchasima Province (stat_m65 file). https://stat.bora.dopa.go.th/new_stat/webPage/statByYear.php

Panmarerng Berk, K. (2003). Financial Accounting. Top.

Phadungsit, M. (2019). Cost accounting (9th ed.). Physics Center.

Phajongwong, P. (2006). Accounting for management. Saengdao.

Phutsa Subdistrict Municipality, Mueang District Nakhon Ratchasima Province. (2021). Local development plan 2023-2027, Change No. 1. http://www.pudsa.go.th/news/doc_download/1แผนพัฒนาท้องถิ่น%20พ.ศ.2566-2570%20เปลี่ยนแปลง%20(ฉบับที่%201)_210623_120928.pdf

Pichetkul, N. (2015). Financial reporting and analysis (5th ed.). Rajamangala University of Technology Thanyaburi.

Rattantraiphop, P. (2018). Principles of cost accounting. Faculty of Business Administration, Kasetsart University.

Rodwanna, P. (2013). Cost Accounting Principles and Processes. Julalongkorn University Press.

Secretary of the One Subdistrict Administrative Committee One National Product. (2020). Action plan to drive the project One Subdistrict One Product year 2019-2022. Secretary of the One Subdistrict Administrative Committee One National Product. https://cep.cdd.go.th/wp-content/uploads/sites/108/2020/06/OTOPActionPlan62.pdf

Strategic Management Group, Lower Northeastern Province Group 1. (2023). Volume reporting the objectives and future development directions of the group of provinces (2023-2027). Office of Strategic Management Lower Northeastern Province Group 1. http://www.osmnortheast-s1.moi.go.th/plan_develop.php

Thongsukowong, A. (2016). Cost accounting. SE-Education.

Thuwanimitrakul, P. (2020). Business Finance (11th ed.). Thammasat University.

Tirakanan, S. (2006). Creating tools to measure variables in social science research: guidelines for practice. Chulalongkorn University Printing House.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2024 Research and Development Institute, Nakhon Ratchasima Rajabhat University

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.