Auditor's Code of Ethics and Reliability in Auditing that Influences the Quality of Audit Work of Certified Public Accountants in Thailand

DOI:

https://doi.org/10.14456/nrru-rdi.2024.21Keywords:

Code’s Ethics, Reliability, Audit QualityAbstract

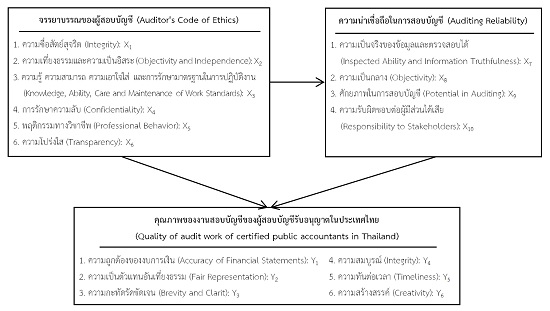

Background and Objective: Supervision, control, supervision and inspection are considered the main elements of good governance that are effective for success in accounting work. Therefore, this research aims to study the ethics of auditors and the reliability of auditing. It influences the quality of audit work of certified public accountants in Thailand.

Methology: Conducting research according to quantitative research methods using survey research methods. A sample of 400 people used a simple random sampling method. The reliability of the questions in the questionnaire is between 0.770-0.978 for use in collecting data via electronic mail ( E-mail ) using inferential statistics to test hypotheses by means of relationship testing. and multiple regression analysis.

Results: Auditor's Code of Ethics regarding Objectivity and Independence Professional behavior Transparency. It influences the reliability of auditing. Able to predict 76.70 percent , followed by reliability in auditing. The truth of the information and can be verified Responsibility to stakeholders Neutral side Influence on the quality of audit work. In terms of fair representation The forecast was 71.10% and the auditor's ethics regarding objectivity and independence. Professional behavior Transparency It influences the quality of the audit work regarding the accuracy of the financial statements. The prediction was 61.10% with statistical significance at the 0.05 level.

Discussion: An important characteristic of ethics involves objectivity. Independent conduct and have good transparency in auditing This allows auditors to use it to find reliable methods for examining financial information and use it in considering improving accounting standards to gain concrete acceptance from consumers and businesses.

Suggestion: Factors affecting the development of creativity for CPAs in Thailand should be studied in order to develop audit practitioners with reliable quality, such as professional skills, skills in using digital technology. Accounting analytical skills and communication skills, etc.

References

Accounting Analysis. (2020). In 2020, has the number of CPAs increased? : Comparing the number of legal entities and auditors. https://www.accounting-analysis.com/2563-cpa/#:~:text=.-,จำนวนผู้สอบบัญชีรับอนุญาต%20(ประเทศไทย)%ที่ยังคง.

Al-Qudah, A. A., Hamdan, A., Al-Okaily, M., & Alhaddad, L. (2023). The impact of green lending on credit risk: Evidence from UAE’s banks. Environmental Science and Pollution Research, 30(22), 61381-61393.

Best, J. W. (1977). Research in Education (3rd ed.). Prentice Hall.

Bills, K. L., Cobabe, M., Pittman, J., & Stein, S. E. (2020). To share or not to share: The importance of peer firm similarity to auditor choice. Accounting, Organizations and Society, 83, 101115. https://doi.org/10.1016/j.aos.2020.101115

Carp, M., & Istrate, C. (2021). Audit quality under influences of audit firm and auditee characteristics: evidence from the Romanian regulated market. Sustainability, 13(12), 6924. https://doi.org/10.3390/su13126924

Glass, G. V., & Hopkins, K. D. (1984). Statistical methods in education and psychology (2nd ed.). Prentice-Halll.

Hair, J. F., Black, W. C., Babin, B. J. & Anderson, R. E. (2010). Multivariate data analysis (7th ed.). Pearson Education.

Hair, J. F., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2014). A Primer on Partial Least Squares Structural Equation Modeling. Sage.

Hamdallah, M. E., Al-N’eimat, S., Srouji, A. F., Al-Okaily, M., & Albitar, K. (2022). The effect of apparent and intellectual sustainability independence on the credibility gap of the accounting information. Sustainability, 14(21), 14259.

Khalil, M. T., Ahmad, N., & Nafees, B. (2024). Impact of Auditors' Attributes on the Identification of Creative Accounting Practices in Pakistan. Contemporary Issues in Social Sciences and Management Practices, 3(1), 27-41. https://doi.org/10.61503/cissmp.v3i1.108

Kiatkrajai, M., & Srichanphet, S. (2004). Accounting Theory (10th ed., Revised edition). TPN Place.

May-Amy, Y. C., Han-Rashwin, L. Y., & Carter, S. (2020). Antecedents of company secretaries’ behaviour and their relationship and effect on intended whistleblowing. Corporate Governance: The International Journal of Business in Society, 20(5), 837-861. DOI 10.1108/CG-10-2019-0308

Ngesti, M., & Djamil, N. (2024). Government Auditors' Capabilities to Detect Fraud and The Factors that Influence Them. InJEBA: International Journal of Economics, Business and Accounting, 2(1), 59-75. https://doi.org/10.5281/zenodo.10802822

Olojede, P., Erin, O., Asiriuwa, O., & Usman, M. (2020). Audit expectation gap: an empirical analysis. Future Business Journal, 6, 1-12. https://doi.org/10.1186/s43093-020-00016-x

Pengjinda, S. (2022). Professionalism and Quality of Audit Services Affecting Service Decision Process for Selecting Audit Firms of Public Company Limited. Rajapark Journal, 16(46), 356-373.

Phiboon, S. ( 2009 ). Training documents for research and academic development courses. Sukhothai Thammathirat Open University.

Regulations of the Accounting Profession No. 19 on the Code of Ethics for Accounting Professionals 2010. (2010, November 3). Royal Gazette. Volume 127, special section 127 D, pages 68-74.

Rezaei, M., Fallah, R., Maranjory, M., & Rostami Mazoee, N. (2024). Provide a structural model of audit quality based on the impact of auditing professional ethics and the moderating role of organizational culture. International Journal of Nonlinear Analysis and Applications, 15(2), 285-299. 10.22075/IJNAA.2022.28947.4029

Saiyot, L., & Saiyot, A. (2000). Learning Assessment Techniques (2nd ed.). Suwiriyasan.

Saudagaran, S. M. (2009). International accounting: A user perspective. CCH.

Sinaga, I. R., Sondakh, J. J., & Warongan, J. D. (2024). The influence of independence, integrity, professionalism, and objectivity on fraud prevention in auditors with auditor ethics as a moderating variable: Empirical study at the Representative Office of the Supreme Audit Agency in North Sulawesi Province. The Contrarian: Finance, Accounting, and Business Research, 3(1), 41-52. https://doi.org/10.58784/cfabr.135

Thammasat Consulting Networking and Coaching Center. (2022). Complete Report (Executive Summary Report) Project to encourage relevant stakeholders to see the value of auditing work. https://www.sec.or.th/TH/Documents/Seminars/seminar-021265-03.pdf

The Comptroller General's Department. (2022). Auditor's report and financial report Office of the Auditor General of the Soil Planning For the year ending 30 September 2023. State Audit Office of the Kingom of Thailand. https://www.audit.go.th/sites/default/files/document/รายงานของผู้สอบบัญชีและรายงานการเงิน%2030%20กย%2066.pdf

The Council of Professional Accountants under Royal Patronage. (2021). Amendments to the Professional Standards for Auditing to be in line with the amendments to the Code of Ethics for Accountants. Auditing Standards 2022. https://acpro-std.tfac.or.th/test_std/uploads/files/TSA/มาตรฐานการสอบบัญชี%20(ประกาศ)/2565_ConformingIESBA.pdf

The Council of Professional Accountants under Royal Patronage. (2022). Handbook of the International Code of Ethics for Professional Accountants Including International Independence Standards 2022 edition. International Federation of Accountants.

Wongwanich, S., & Wiratchai, N. (2003). Guidelines for thesis counseling. Chulalongkorn University.

Yamane, T. (1973). Statistics: an introductory analysis (2nd ed.). Harper & Row.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2024 Research and Development Institute, Nakhon Ratchasima Rajabhat University

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.