The Study and Improvement of Cost Accounting System Employing Participatory Action Research for System to Support Job Order Costing: A Linoleum in Nakhon Pathom Province

DOI:

https://doi.org/10.14456/rc-sdj.2025.14Keywords:

cost accounting system, participatory action research, make-to-order, linoleum businessAbstract

Background: Job-ordered production requires accurate cost data that is consistent with the actual manufacturing process. This research aims to enhance the current cost accounting system and design, and propose improvements in cost accounting for job-ordered production.

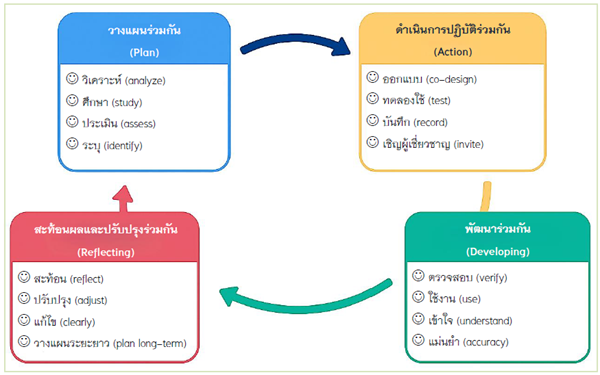

Methods: Participatory action research using a linoleum factory in Nakhon Pathom Province as a case study. Five purposively selected informants were selected: business owners, production managers, production line supervisors, accounting supervisors, and cost accounting staff. The instrument used was an open-ended structured interview form. The questions were divided according to the informants' roles. Data collection was based on action research concepts, including in-depth individual interviews and informal observations. A workshop on creating a cost accounting system for custom-made work was also organized. Data were analyzed using content analysis, with cost accounting principles serving as a framework, and a data flow diagram was created. For the analysis of variable and fixed cost data, the percentage and sum methods are used, while Cost allocation uses the multiplication method.

Results: The business has seen a decrease in sales and therefore has to reduce production capacity. The business owner wants to use the remaining production capacity to generate income by accepting orders from customers. The current cost accounting system is a continuous production system, which is different from the job-to-order cost accounting system. Therefore, the problem must be studied and redesigned. In designing the new system, a job order form is designed, a new data flow is defined, and it is recommended to allocate costs based on the number of hours produced per order.

Conclusions: The research designed a new cost accounting system to support production orders from customers. This involves calculating production costs for each customer's order. The new cost accounting system is suitable for accepting orders for oilcloth production according to the quantity and quality specified by the customer. It enables the collection of complete and accurate cost data, which will help business owners set prices from customers and achieve appropriate profits.

References

Department of Alternative Energy Development and Efficiency. (2005). Knowledge Guide/Department of Alternative Energy Development and Efficiency (DEDE). Ministry of Energy.

Deshmukh, S., Sakgaibjarm, A., & Harichandan, D. (2017). Cost & Management Accounting System. University of Mumbai.

Dockery, M. (2025). A Process Perspective: Proven Approaches to Quality Adoption and Process Integration for Business. Newman Springs Publishing.

Dolsuk, S., & Lojnsirisilp, D. (2025). Improving Cost Accounting System of a Peanut Processing Community Enterprise in Yasothon Province. Phetchabun Rajabhat Journal, 27(1), 59-66.

Horngren, C. T., Datar, S. M., & Rajan, M. V. (2015). Cost Accounting A Managerial Emphasis (15th ed). Pearson Education.

Inthapantee, P., Suknu, P., Jantawong, J., & Nuanlaong, P. (2023). Accounting System Development and Production Cost Management to Enhance Community Products of Occupation Promotion Community Enterprise Group at Ban Nikhom, Muang District, Surat Thani Province. The Journal of Research and Academics, 6(4), 145-162.

Junpitu, Y., Narin, C., Chinnawong, N., Meechai, R., Nonsiri, S., Nonghanpitak, K., & Jantala, J. (2024). A Study of Current Situations, Problems and Obstacles of Bookkeeping to Accounting System Development of Community Enterprises’s Weaving Group Ban Sam Thor, Saeng Sawang Subdistrict, Nong Saeng District, Udon Thani Province. Santapol College Academic Journal, 10(1), 1-11.

Khapanyo, A. (2006). Principles of Program Design and Development. Success Media.

Komaratat, D. (2016). Cost Accounting (15th ed.). Chulalongkorn University Press.

Majumder, R. Q. (2025). The Role of Cost Accounting Data in Enhancing Manufacturing Efficiency. International Journal of Research and Innovation in Social Science (IJRISS), IX(VII), 1121-1133. https://dx.doi.org/10.47772/IJRISS.2025.90700091

McTaggart, R. (2010). Participatory action research or change and development. James Cook University.

Memarpour, E., & Torabi, S. A. (2025). Integrated sales and operations planning for a multi-channel, hybrid make-to-stock/make-to-order tire supply chain. Journal of Industrial and Production Engineering, 1-22. https://doi.org/10.1080/21681015.2025.2484388

Mertler, C. A. (2019). The Wiley handbook of action research in education. John Wiley & Sons.

Pimta, L., & Serichai, C. (2025). Modern Accounting Competency Affecting the Financial Reporting Quality of Company Accountants in the Northeast Region. Arts of Management Journal, 9(3), 247-269.

Romney, M. B., & Steinbart, P. J. (2016). Accounting information systems (14th ed.). Pearson.

Stoecker, R., & Falcón, A. (2022). Handbook on Participatory Action Research and Community Development. Edward Elgar.

Suriyaphiwat, W. (2010). Basic Computers and Programming Techniques. Chulalongkorn University Press.

Thankarn, J. (2023). Accounting System Design for Small Business: A Case of Satay AAA [Independent Study, Thammasat University].

Ueajirapongphan, S. (2009). Cost Accounting 1: Concepts in calculating product costs and accounting principles. McGraw-Hill.

Ueajirapongphan, S. (2009). Management Accounting. McGraw-Hill.

Usul, H., & Olgun, E. B. (2025). An analysis of material flow cost accounting in companies using different cost accounting systems. Heliyon, 11(4), e42555.